FINTECH

Fintech GTM in MENA: Why Localized Super Apps Succeed

April 12, 2026 • 24 Min Read

Fintech GTM in MENA: Why Localized Super Apps Succeed

Lifting and shifting Western or Asian models won’t work in the Middle East. Here is how to navigate regional remittance habits, complex eKYC, and digital trust to build a winning market entry.

Fintech Super-App Success in MENA

The “Lift and Shift” Fallacy: Why Western and Asian Frameworks Fail in MENA

In early 2023, Astra Tech, a UAE-based technology group, made a move that confused plenty of traditional product managers: they bought Botim.

To a fintech executive sitting in London or Silicon Valley, acquiring a VoIP voice-calling app to build a financial Super App makes very little sense. But in the UAE, it was a masterclass in cultural engineering. Astra Tech recognized a demographic reality that Western frameworks completely miss: millions of blue-collar expatriates in the GCC use Botim every single day to call their families in Bangladesh, India, and Pakistan.

Astra didn’t try to build a sleek, minimalist neo-bank from scratch and beg users to download it. Instead, they went to where the users already were. They bought the exact moment of emotional and financial connection, integrating remittance and digital wallet features directly into the daily habit of calling home. Today, Botim operates as the region’s premier “Ultra App,” processing millions in cross-border payments.

Compare that to the heavily funded European giants. Revolut, despite its massive global valuation and success in the West, spent years navigating regulatory and market complexities in the Middle East, only managing to secure an in-principle payment license in the UAE by late 2025.

This stark contrast highlights the danger of the “lift and shift” fallacy. Too often, product leaders look at the success of Monzo in the UK or WeChat in China, package those exact features into a cloned app, and assume they have a winning Go-To-Market (GTM) strategy for Dubai or Riyadh.

It simply does not work. You cannot copy-paste a generalized framework into a region governed by such polarized demographics. The UAE market is defined by a massive expatriate workforce operating directly alongside a highly affluent local citizen population. An “all-in-one” lifestyle app designed primarily to split Friday brunch bills in Downtown Dubai entirely bypasses the actual engine of the region’s digital economy: the expat standing in line at a physical exchange house in Deira, desperate for a low-cost, frictionless way to send money home.

What drives engagement today in Europe or Asia will not automatically capture the MENA user of tomorrow. Building a successful ecosystem here requires architecting a product that respects these divided financial habits right out of the gate. If your GTM strategy isn’t engineered for this specific cultural reality, your launch budget is already wasted.

Cultural Engineering in Action: The Cross-Border Remittance Hook

If you look at the evolution of Super Apps globally, they all rely on a “Trojan Horse” — a high-frequency, daily-use service that gets the app installed on a user’s phone, building the necessary trust to cross-sell financial products later.

In Southeast Asia, that Trojan Horse was ride-hailing (Grab). In Latin America, it was food delivery (Rappi). But in the GCC, trying to use lifestyle logistics as your primary user acquisition engine is a fast track to burning venture capital. The market is already saturated, and user loyalty is bought entirely through discount codes.

In the Middle East, the ultimate acquisition hook is much more foundational: the cross-border remittance corridor.

Consider the billions of dollars flowing annually from the UAE to India, Bangladesh, and Pakistan. For decades, legacy giants like Al Ansari Exchange built absolute empires out of brick-and-mortar branches because they offered tangible, physical trust. But true “cultural engineering” in a digital app means understanding that an expat is not just sending money to a generic “bank account.” They are sending it to a highly specific, local financial ecosystem back home.

If you are building a Super App for the UAE today, your product team must engineer direct endpoints into South Asia’s dominant payment rails:

- The India Corridor: You aren’t just facilitating a wire transfer; you are integrating directly with UPI (Unified Payments Interface). The most successful GTM strategies right now leverage the interoperability between the UAE’s Aani network and India’s UPI, allowing an Indian expat in Dubai to instantly remit funds directly to their family’s PhonePe or Google Pay wallet in Kerala, using just a phone number.

- The Bangladesh Corridor: A massive portion of the Bangladeshi expat workforce in the GCC sends money to families in semi-urban or rural areas where traditional banking penetration is low. A successful MENA Super App doesn’t ask for routing numbers; it features a native “Send to bKash” or Nagad integration. When an app connects a Dubai salary directly to a bKash agent point in Sylhet or Dhaka in under 60 seconds, the app has won that user’s loyalty forever.

- The Pakistan Corridor: Similarly, Pakistani expats are increasingly moving away from legacy cash agents. The winning digital wallets in the UAE are tapping directly into the State Bank of Pakistan’s Raast instant payment system or integrating with EasyPaisa and JazzCash.

When startups like e& money or HubPay aggressively capture market share, it is because they engineered these exact corridors. They understood that their primary competitor wasn’t another digital bank; it was a 45-minute wait in the Dubai summer heat at a physical exchange house.

Strategically, this remittance engine should not be viewed merely as a product feature — it is your Customer Acquisition Cost (CAC) subsidy.

This is where the “built for today, engineered for tomorrow” mindset becomes critical. You engineer the UPI or bKash remittance flow to solve today’s immediate problem. But every time that user safely routes their salary through your pipes, they are granting you digital trust. More importantly, they are handing you a consistent, verifiable ledger of their financial behavior.

That transaction data is the goldmine for tomorrow. The localized remittance flow you build today becomes the proprietary credit-scoring model you will use tomorrow to confidently upsell that exact same user on micro-lending, health insurance, or wealth management. In the MENA region, if you do not own the remittance flow today, you will not own the user tomorrow.

The Onboarding Paradox: Frictionless eKYC vs. Institutional Security

In the fintech world, user onboarding is the exact place where Go-To-Market budgets go to die.

There is an inherent paradox in launching a financial app: the Growth team wants a frictionless, two-click sign-up process to maximize conversion rates, while the Compliance team demands a fortress of identity verification to satisfy the Central Bank. If you bring a Western “rapid onboarding” playbook into the MENA region, your app will either be crippled by massive drop-off rates or shut down for compliance breaches.

True cultural engineering in the UAE means deeply integrating with the local identity infrastructure rather than forcing a proprietary verification system.

The undisputed gold standard for this today is the UAE Pass and the Emirates ID (EID). When a European or Asian fintech enters the market, they often rely on generic Optical Character Recognition (OCR) vendors to scan passports. But for a blue-collar expat standing in a poorly lit room trying to scan an old document, generic OCR fails frequently. Every failed scan is a frustrated user who deletes the app and walks back to the physical exchange house.

The successful GTM players architect their onboarding flow around the Emirates ID. By integrating directly with the UAE Pass or utilizing NFC-based EID reading, the data entry friction drops to near zero.

But pulling data is only half the battle; proving the human is the other.

With the democratization of generative AI, the threat of Deepfake identity injection is keeping regional compliance officers awake at night. A standard “take a selfie” feature is no longer enough to satisfy a Central Bank audit. To launch successfully today, your eKYC pipeline must integrate advanced, AI-driven Liveness Verification. It must passively map micro-expressions, detect screen glare, and measure the spatial depth of a face in real-time. The system has to definitively prove that a living, breathing human is holding the device — not a 3D-rendered mask, a high-res photo, or an AI-manipulated video stream injected directly into the camera feed.

Resolving this paradox is how you build for today while architecting for tomorrow.

Today, a localized eKYC flow that seamlessly reads an Emirates ID while running imperceptible deepfake checks stops user drop-off and prevents synthetic identity fraud. But tomorrow, that deeply verified, government-backed identity graph becomes your ultimate commercial asset. When the UAE fully rolls out comprehensive Open Banking regulations, the platform that holds the most secure, frictionless, and compliant identity layer will be the one authorized to instantly pull a user’s salary history and underwrite a micro-loan in real-time.

You do not win the market by bypassing security; you win by making military-grade compliance invisible to the user.

The Zero-Tolerance Gatekeeper: 100% Central Bank Compliance

In Silicon Valley, the classic startup mantra is “move fast and break things.” In the Middle Eastern fintech sector, if you break a Central Bank mandate, your board gets a phone call, your operations freeze, and your license is revoked.

Regulators like the Central Bank of the UAE (CBUAE) and the Saudi Central Bank (SAMA) do not treat compliance as a suggestion; they treat it as a zero-tolerance baseline. To put this into commercial perspective: in July 2025 alone, the CBUAE levied AED 4.1 million in financial sanctions against three exchange houses, and fined a local bank AED 3 million simply for failing to maintain robust AML/CFT (Anti-Money Laundering and Combating the Financing of Terrorism) frameworks.

Furthermore, with the introduction of the new UAE Federal Decree-Law №10 of 2025, the burden of proof for prosecuting financial crimes was significantly lowered. The regulatory environment is only getting stricter. Fulfilling 100% of these mandates is no longer just a legal necessity — it is your Go-To-Market speed limit.

For a localized Super App processing millions of cross-border micro-transactions to markets like Bangladesh, India, or Pakistan, standard “out-of-the-box” Western compliance software will fail you.

The biggest operational bottleneck for a scaling fintech here is an uncalibrated Transaction Monitoring (TM) system. If your rules engine is too rigid, it flags every legitimate remittance as suspicious, resulting in a tsunami of “False Positives.” Your operations team drowns in manual reviews, and users abandon the app because their transfers are delayed by 48 hours. Conversely, if your system is too loose, you become a conduit for illicit funds and guarantee a CBUAE audit.

True cultural engineering requires a localized, AI-driven TM rules engine. It needs to autonomously recognize that a sudden 300% spike in AED 800 transfers to South Asia during the week before Eid is a predictable, culturally driven demographic behavior, not a coordinated money-laundering syndicate.

This is where the separation between “launching today” and “surviving tomorrow” becomes painfully obvious.

Today, 100% compliance means hitting the baseline: seamless API integrations with global sanction lists, localized PEP screening, and automated Suspicious Transaction Report (STR) generation.

But tomorrow, the regulatory ground is shifting entirely toward blockchain and programmable money. Under its Financial Infrastructure Transformation (FIT) programme, the UAE has already codified the Digital Dirham as legal tender. We aren’t just talking about pilot phases anymore; through Project mBridge, the CBUAE has already successfully executed cross-border CBDC transactions (such as a massive AED 50 million transfer to China) that bypassed the traditional correspondent banking network entirely, reducing settlement times from days to seconds.

If your backend compliance architecture is a hardcoded monolith, adapting your TM systems to monitor programmable CBDC smart contracts will require a multi-million dollar, year-long rebuild. But if you have built your regulatory tech to be modular and API-first today, accommodating the Digital Dirham tomorrow isn’t a crisis; it is just your next sprint. You secure the market today by satisfying the auditor, and you dominate tomorrow by out-pacing your competitors when the monetary rails fundamentally change.

The B2B2C Backbone: Empowering Merchant and Agent Networks

There is a fatal flaw in how many digital-first teams approach GTM in the Middle East: they treat physical distribution as a relic of the past. They pour millions into B2C performance marketing — bidding aggressively on Google and Facebook ads — hoping to force app downloads.

But a Super App cannot survive purely on a B2C acquisition model. While the GCC boasts smartphone penetration rates exceeding 90%, the World Bank estimates that nearly 50% of the broader MENA adult population remains unbanked or severely underbanked. For this massive demographic, digital trust is still mediated by physical proximity and cash.

If your GTM strategy ignores the physical ground game, you are leaving your most effective customer acquisition channels on the table.

You do not have to look far to see the mathematical proof of this. Look at Fawry in Egypt. They did not reach a multi-billion dollar valuation and capture over 50 million users just by launching a sleek consumer app. They won the market by deploying a B2B2C backbone, transforming over 300,000 local merchants and kiosks into a decentralized network of cash-in/cash-out (CICO) agents.

Similarly, in the UAE, there are an estimated 10,000+ baqalas (neighborhood grocery stores). These micro-merchants are the established community touchpoints for the blue-collar workforce. The winning play is to turn these local shops into your frontline onboarding agents.

However, the reason many Western-engineered fintechs fail at this is technical arrogance. They build an incredible consumer app, but when it comes to the merchant side, they deploy a clunky, over-engineered dashboard that requires a computer science degree to navigate.

To secure the commercial bottom line, you must deploy an intuitive Merchant and Agent platform specifically designed for non-technical users.

This is where the architecture of the platform dictates commercial scale. By embedding a highly simplified, integrated Content Management System (CMS) directly into the merchant portal, you empower ground-level operational staff. A regional sales manager or a local shop owner in Deira should be able to instantly launch a hyper-local cashback promotion, update their service catalog, or resolve a failed top-up without ever needing to submit a Jira ticket to your core engineering team.

When you remove the technical bottleneck from your field operations, your distribution scales exponentially.

This strategy perfectly encapsulates the “build for today, architect for tomorrow” mandate.

Today, empowering that network of 10,000 baqalas with a frictionless platform turns them into an aggressive, low-cost acquisition engine for your Super App, driving down your B2C marketing burn rate. But tomorrow, that merchant network is no longer just a distribution channel — it is your B2B lending pipeline. Because you have been processing their daily transaction velocity, you now have the exact ledger required to underwrite and offer them instant working capital loans or merchant cash advances.

You use the agent network to capture the consumer today, and you monetize the agent’s business growth tomorrow.

The Ecosystem Moat: Strategic Partnerships & Integrations

There is a hard truth about scaling a fintech product in the MENA region: you cannot build a “Super App” in a silo. If your entire strategy relies on users proactively opening your app just to manage their money, you are already losing to the incumbents.

True scale requires embedding your financial infrastructure into the daily, unavoidable habits of the consumer. In the Gulf, the ultimate competitive advantage isn’t a flashier UI; it is an unbreachable ecosystem moat built through strategic partnerships.

Look no further than Barq, the Saudi digital wallet launched by former STC Pay CEO Ahmed Alenazi. In a market seemingly dominated by massive telecom-backed wallets, Barq managed to shatter all regional acquisition records — hitting 1 million users in just 21 days after its 2024 launch, and crossing an astonishing 10 million users within its first 17 months.

How did a newcomer pull that off? They didn’t just build a wallet; they built a heavily integrated ecosystem.

First, Barq established a massive commercial advantage by securing a SAMA (Saudi Central Bank) license that allowed for a monthly transfer limit of SAR 100,000 — five times higher than the SAR 20,000 limit of traditional competitors. But the true genius was in their partnerships. They didn’t try to build their own global payment rails from scratch. Instead, they forged immediate, high-level integrations with Thunes and Western Union, instantly connecting Barq users to billions of mobile wallets and bank accounts across 200 countries.

Furthermore, they integrated deeply into the B2B physical economy. By partnering with companies like Geidea, Barq enabled point-of-delivery digital payments, seamlessly weaving their app into the Saudi e-commerce and logistics ecosystem. When a consumer uses Barq to pay for a delivery at their doorstep, and then uses that same app to remit their salary home globally in real-time, the app ceases to be a mere financial tool — it becomes a daily operational necessity.

Similarly, we see this ecosystem mastery in the UAE. Consider e& money’s massive strategic play to become the UAE’s first digital wallet linked directly to PayPal for instant AED withdrawals. To a traditional banker, this might just look like an API integration. But to a Growth Leader, it is a monopoly. By eliminating the cross-border friction for thousands of UAE-based freelancers and digital creators, e& money didn’t just launch a feature — they monopolized a lucrative demographic.

This is the essence of building for today while architecting for tomorrow.

Today, integrating heavily with global payment gateways (like PayPal or Thunes), physical logistics networks, and regional telecom providers secures your user retention.

But tomorrow, that deeply integrated ecosystem lock-in becomes your ultimate commercial moat. As the Saudi and UAE markets aggressively push toward Vision 2030 and a 70% non-cash economy, standalone digital banks will struggle to survive. The platforms that have already embedded themselves into the consumer’s daily life — like Barq and e& money — will naturally become the default distributors for tomorrow’s high-margin products: contextual health insurance, auto-lending at the point of sale, and automated wealth management.

Escaping the Monolith: Why Microservices are Mandatory for Regional Expansion

So far, we have discussed commercial strategies, cultural empathy, and regulatory moats. But none of these frameworks survive contact with the market if your underlying codebase is a liability. In fintech, technical debt is not just an engineering problem; it is a Go-To-Market killer.

Many ambitious digital wallets launch in their home market built on a monolithic architecture. It is fast, cohesive, and gets the MVP out the door. But when it is time to expand — say, taking a successful UAE app into Saudi Arabia, Africa, or the UK — the monolith becomes a straightjacket.

In a tightly coupled monolith, changing a single line of code to satisfy a new SAMA compliance rule in Riyadh could inadvertently break the onboarding flow in Dubai. Your engineering cycles drag from weeks to months, and your GTM launch is paralyzed by regression testing. You cannot future-proof a legacy monolith.

The only way to achieve true regional scale is by architecting for modular agility.

In practice, migrating a legacy system from a monolithic architecture to microservices is what actually allows a product team to ship 15+ localized features in a single quarter without risking total system collapse. It changes the entire commercial trajectory of the product.

When you decouple your architecture, you separate your “Core” from your “Context.”

Your Core Ledger — the absolute truth of user balances, debits, and credits — remains stable, highly secure, and untouched. Surrounding this core are your localized microservices: a specific eKYC module for the UAE Pass, a distinct transaction monitoring module for Saudi compliance, and a dedicated integration service for UK Open Banking APIs.

This modularity is the ultimate regional growth hack.

It means that when you decide to expand from the GCC into the UK market, you do not have to rebuild your entire banking platform. You keep the core ledger intact, spin up a new instance, and simply swap out the local microservices. You plug in a UK-specific identity verification module and an FPS (Faster Payments Service) gateway, and suddenly, you are operational in a new continent.

This brings us back to the “built for today, architected for tomorrow” mandate.

Today, a microservices architecture protects your commercial bottom line by ensuring that your UAE operations remain resilient and agile, allowing you to deploy new localized features (like a bespoke merchant CMS) without downtime.

But tomorrow, that same architecture becomes your expansion engine. When the executive board decides to target the African remittance corridor, your engineering team isn’t starting from scratch. They are simply building a new localized “spoke” to connect to your existing hub. You secure your home market today, and you architect the modular agility required to conquer new regions tomorrow.

Growth Analytics: Moving Beyond Vanity Metrics

There is a specific metric that has killed more fintech Go-To-Market strategies than bad code or harsh regulations: the “App Download.”

When a digital wallet launches in the UAE or Saudi Arabia, marketing teams often celebrate hitting 100,000 installs in the first month. But in the commercial reality of fintech, an app install is a pure vanity metric. Even “Monthly Active Users” (MAU) is a dangerously shallow KPI if a user is only opening the app to check their balance without actually moving money.

In the MENA region, the only metric that guarantees survival is Transaction Velocity.

If you are not rigorously tracking how fast and how frequently money moves from a user’s linked bank account, through your wallet, and out to a bKash or UPI endpoint, you are flying blind.

Look at Careem’s transition into the Middle East’s dominant Super App. Careem didn’t reach its decacorn valuation by just tracking how many people opened the app to book a ride. Their Growth Analytics team became obsessed with “Cross-Vertical Utilization.” They rigorously tracked the exact behavioral pathways that led a ride-hailing user to make their first food delivery order, and subsequently, to fund their Careem Pay wallet. By moving past vanity metrics and tracking these deep-funnel events, they engineered an ecosystem where the CAC (Customer Acquisition Cost) for their fintech product was subsidized almost entirely by their mobility product.

We see this same obsession on a global scale with Wise (formerly TransferWise). Wise completely disrupted the UK and global remittance market not just by offering lower fees, but through microscopic behavioral tracking. They didn’t just measure whether a transfer was successful; they measured the milliseconds of friction a user experienced when inputting a beneficiary’s IBAN. They used data to systematically hunt down and eliminate every single point of friction in the user journey, resulting in a product so seamless that word-of-mouth replaced traditional marketing.

To replicate this level of dominance in the MENA market, product teams must abandon generic marketing dashboards and build an event-driven data pipeline.

The Engine: GA4 & BigQuery

The winning GTM strategies rely on a highly specific stack. Google Tag Manager (GTM) fires custom events for every micro-interaction, which are collected by GA4.

However, GA4 alone is not enough — it is a reporting tool, not a data warehouse. True growth leaders pipe that raw, unfiltered GA4 data directly into Google BigQuery.

Why is BigQuery the game-changer here? Because it allows your data team to run complex SQL joins that merge your front-end behavioral data with your backend commercial data. For example, BigQuery allows you to take a specific Facebook Ad ID from a campaign targeting Indian expats and track that exact cohort’s remittance volume three months later. You are no longer guessing your Return on Ad Spend (ROAS); you can mathematically prove the exact Lifetime Value (LTV) of a user acquired through a specific channel.

Beyond the Click: Tracking Actual User Behavior

But quantitative data (the “what”) only tells half the story. To engineer a truly localized app, you must also capture qualitative data (the “why”).

If BigQuery tells you that 30% of users drop off at the Emirates ID scanning screen, you need Product Analytics to understand why.

- Behavioral Analytics (Amplitude or Mixpanel): These tools go deeper than GA4. They allow product managers to build complex retention curves and cohort analyses on the fly. You can instantly see if users who complete their first remittance within 24 hours of onboarding are 5x more likely to remain active after 90 days.

- Qualitative Tracking (Hotjar or Microsoft Clarity): This is where you see the human element. By utilizing session recordings and heatmaps, you can actually watch anonymized user sessions. You might discover that the 30% drop-off at the eKYC stage isn’t a technical bug, but rather users “rage-clicking” on an improperly translated Arabic instruction button that is slightly off-screen on older Android devices.

Data without immediate operational action is just trivia.

This brings us to the final application of the “built for today, architected for tomorrow” mindset.

Today, utilizing the GA4, BigQuery, and Amplitude stack allows you to plug the invisible leaks in your acquisition funnel, immediately lowering your CAC and driving daily revenue.

But tomorrow, that massive warehouse of transactional and behavioral data becomes your predictive engine. By analyzing the historical velocity of a blue-collar expat’s transfer habits, your system won’t just track when they remit money — it will predict it. You will push a highly personalized, zero-fee remittance offer to their phone exactly 12 hours before they traditionally get paid, effectively locking out your competitors before the user even opens the app.

You capture the data to survive today; you weaponize the data to dominate tomorrow.

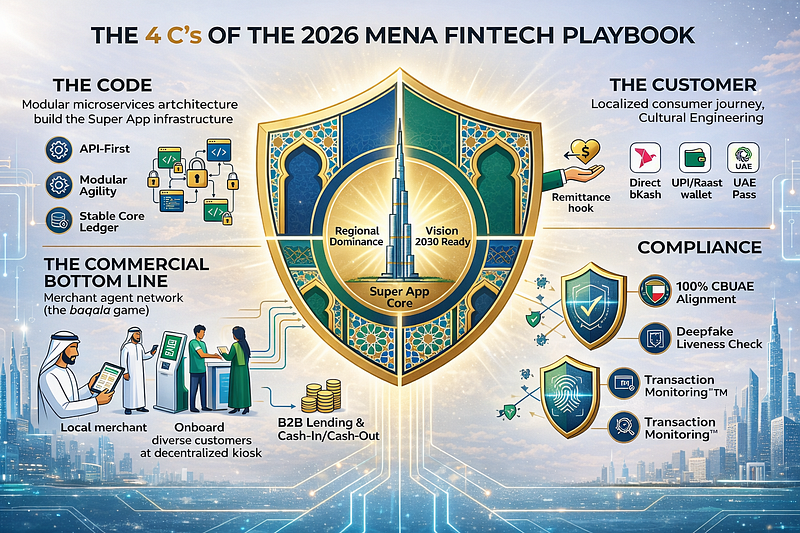

The 4 C’s of the 2026 MENA Fintech Playbook

4C’s of MENA Playbook — Image created using AI

The era of easy venture capital subsidizing bloated user acquisition in the Middle East is over. The next generation of fintech dominance will not be won by the team with the sleekest UI or the most aggressive YouTube ad spend. It will be won by the teams who treat Go-To-Market not as a marketing function, but as an architectural mandate.

Lifting and shifting a Western or Asian Super App model into Dubai or Riyadh is a guaranteed recipe for failure. To genuinely capture and monetize the complex demographic realities of the MENA region, product and growth leaders must ruthlessly execute across four uncompromising pillars:

- The Code (Modular Agility): Technical debt is commercial death. You cannot future-proof a legacy monolith. By migrating to an API-first, microservices architecture, you secure the stability of your core ledger in your home market today, while maintaining the agility to rapidly swap localized modules for expansion into Africa or the UK tomorrow.

- The Customer (Cultural Engineering): You must respect the demographic divide. For the massive expatriate workforce, lifestyle features are irrelevant; the cross-border remittance corridor is your true acquisition hook. You win their loyalty by seamlessly integrating with their home-country payment rails (UPI, bKash, Raast) and solving their most acute daily friction.

- The Commercial Bottom Line (The B2B2C Backbone): A localized Super App cannot survive purely on B2C app downloads. You must capture the physical ground game. By deploying an intuitive, CMS-powered merchant platform, you transform the neighborhood baqalas and kiosks into your decentralized onboarding agents and future B2B lending pipeline.

- Compliance (The Zero-Tolerance Gatekeeper): Regulatory tech is your GTM speed limit. Fulfilling 100% of Central Bank mandates — from frictionless Emirates ID reading and deepfake-proof liveness checks to localized transaction monitoring — is non-negotiable. Making military-grade compliance invisible to the user is how you secure digital trust and prepare for the imminent shift toward Open Banking and CBDCs.

The MENA fintech landscape in 2026 will be unforgiving to generic solutions. The winners will be those who understand that true product growth sits at the exact intersection of local empathy, ecosystem partnerships, and rigorous data analytics.

You do not build a Super App for the Middle East by copying what worked elsewhere. You build it by engineering exactly what the region needs today, while architecting the infrastructure to own tomorrow.

References & Real-World Cases

- Astra Tech & Botim Acquisition (UAE): https://yourstory.com/ys-gulf/astra-tech-acquires-voice-calling-app-botim-uae-startups-digital-payments

- Revolut UAE License Timeline: https://en.wikipedia.org/wiki/Revolut

- Aani Network & India Corridor Integration: https://aep.ae/en/news-media/press-releasesarticles/uae-instant-payments-platform-aani-signs-up-15-million-users/

- CBUAE AED 4.1 Million AML Fine: https://www.centralbank.ae/media/hhphe2s3/cbuae-imposes-financial-sanctions-of-aed-4-1-million-on-three-exchange-houses-en.pdf

- Project mBridge (AED 50 Million CBDC Transaction): https://www.ledgerinsights.com/uae-cross-border-cbdc-payment-mbridge/

- Digital Dirham & CBUAE FIT Programme: https://uabonline.org/english-news/uae-makes-first-digital-dirham-transfer-via-mbridge-cbdc-platform/

- Fawry (Egypt) 300,000+ Merchant Network: https://portersfiveforce.com/blogs/brief-history/myfawry

- Barq (Saudi Arabia) 10 Million Users & SAMA Limits: https://en.arageek.com/barq-surges-past-10-million-users-dominates-saudi-fintech-revolution

- Careem Cross-Vertical Utilization: https://uaeceo.com/blog/careem-restructures-super-app-into-vertical-focused-units-to-drive-operational-efficiency

- Careem Digital Acceleration & Core NPS: https://www.netguru.com/blog/digital-acceleration-careem